However, you can also start with the balance as per passbook when preparing a BRS, but the treatment for all outsourced accounting and bookkeeping the items mentioned above shall be reversed. Likewise, ‘credit balance as per cash book’ is the same as ‘debit balance as per passbook’ means the withdrawals made by a company from a bank account exceed deposits made. Deposits in transit, or outstanding deposits, are not showcased in the bank statement on the reconciliation date. This is due to the time delay that occurs between the depositing of cash or a check and the crediting of it into your account.

It’s important to perform a bank reconciliation periodically to identify fraudulent activities or bookkeeping and accounting errors. This way, you can ensure your business is in solid standing and never be caught off-guard. If your beginning balance in your accounting software isn’t correct, the bank account won’t reconcile. This can happen if you’re reconciling an account for the first time or if it wasn’t properly reconciled last month. You should perform monthly bank reconciliations so you can better manage your cash flow and understand your true cash position. Read on to learn about bank reconciliations, use cases, and common errors to look for.

He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University.

Principal that is to be received within one year of the balance sheet date is reported as a current asset. Any portion of the notes receivable that is not due within one year of the balance sheet date is reported as a long term asset. Things that are resources owned by a company and which have future economic value that can be measured and can be expressed in dollars.

NSF check is a check issued by a company, but the bank did not pay/honor the check because the company’s bank balance was less than the amount of the check. An NSF check is also known as a check that “bounced” or as a “rubber check” (since the check is being bounced back by the bank). A bank credit memo is recorded in the bank’s general ledger with a credit to the bank’s liability account Customers’ Deposits (causing this liability’s account balance to increase). The bank also debits its asset account Loans Receivable (causing this asset’s balance to increase). Keeping on top of your bank reconciliation ensures that you’re always aware of your company’s financial situation. This helps you anticipate any cash flow challenges so you can respond appropriately.

Since check #147 is in Ott Company’s general ledger Cash account, but isn’t on the May 31 bank statement, check #147 is an outstanding check that will be an adjustment to the Balance per BANK. Bank debit memos indicate that the bank has decreased the balance in a company’s checking account. Examples include bank fees (service charge, overdraft fee, stop payment fee, etc.) and loan payments. Deposits in transit are the cash and checks a company has received and recorded in its general ledger accounts, but the cash and checks have not been processed by the bank as of the date of the bank reconciliation. Remember that transactions that aren’t accounted for in your bank statement won’t extension of time to file your tax return be as obvious as bank-only transactions. This is where your accounting software can help you reconcile and keep track of outstanding checks and deposits.

Another type of error involves omitting or adding a zero, such as recording $500 instead of the actual amount of $5,000 (a difference of $4,500). Here are two examples to reinforce the bank’s use of debit and credit with regards to its customers’ checking accounts. Before deep diving into the practical examples of bank reconciliation statements, let’s go through a few terminologies which are used in a recurring way while explaining the examples. Once the balances are equal, businesses need to prepare journal entries to adjust the balance per books. Free Excel bank reconciliation statement that will help you match transactions, track your reconciliation, and provide useful formulas and tips.

If the charges are not from your bank, the bank can also help you identify the source so that you can prevent any fraud or theft risk. Through these components, a bank reconciliation template systematically ensures the integrity and accuracy of financial records, facilitating reliable financial management and oversight. There are times when the bank may charge a fee for maintaining your account, which will typically be deducted automatically from your account. Therefore, when preparing a bank reconciliation statement you must account for any fees deducted from your account. There are times when your business will deposit a check or draw a bill of exchange discounted with the bank. These deposited checks or discounted bills of exchange drawn by your business may get dishonored on the date of maturity.

The Cashbook closing balance for the last day of April will remain as $2,091.50. There is still a difference in the Cashbook of $350 which is due to the unpresented check/cheque from Query No. 7. At this stage Rose could also go back to the Bank Statement and tick off the highlighted transactions to show that they have now all been dealt with. Rose dates them all at April 30th (except for No 6. Cash withdrawal) but indicates in the Details column the date of the original transaction entry in the Cashbook. All names of people and businesses in these exercises are fictitious and made up from my imagination.

The bottom line of both sides of the bank reconciliation what is the journal entry for accounts payable must be the same amount. In other words, Adjusted balance per BANK must equal Adjusted balance per BOOKS. Here is the example of Rose’s reconciliation template which shows you how to get the bank reconciliation format correct.

The bank may send you a bank statement at the end of each month, each week, or, if your business has a large number of transactions, they may even send one at the end of each day. You’ll need to adjust the closing balance of your bank statement in order to showcase the correct amount of withdrawals or any checks issued that have not yet been presented for payment. Preparing a bank reconciliation statement is done by taking into account all transactions that have occurred up until the date preceding the day the bank reconciliation statement is prepared. To reconcile your bank statement with your cash book, you’ll need to ensure that the cash book is complete and make sure that the current month’s bank statement has also been obtained.

This process not only enhances financial accuracy but also acts as a critical internal control mechanism for uncovering discrepancies, thereby preventing fraud and identifying potential banking and accounting errors. We’ll explore the definition of bank reconciliation, why it’s important, and a step-by-step process for performing bank reconciliations. We’ll also look at common sources of discrepancies between financial statements and bank statements to help you identify fraud risks and errors. Performing regular bank reconciliations is key to keeping on top of your company’s financial health and paving the way for sustainable business growth. The bank reconciliation statement template is engineered for efficiency, offering a clear, step-by-step framework that simplifies the reconciliation process. Whether you’re overseeing the finances of a business or keeping track of personal bank accounts, this template is versatile enough to meet a wide range of needs.

Since the adjustments to the balance per the BOOKS have not been recorded as of the date of the bank reconciliation, the company must record them in its general ledger accounts. ACH, EFT, Zelle transfers, and wire transfers can indicate additions to or subtractions from a company’s bank account without the company preparing a deposit slip or writing a check. Cancelled checks are the checks the company issued and were paid by the company’s bank. Cancelled checks are also referred to as checks that “cleared” the bank account on which they are drawn.

For each of the adjustments shown on the Balance per BOOKS side of the bank reconciliation, a journal entry is required. Each journal entry will affect at least two accounts, one of which is the company’s general ledger Cash account. Outstanding checks are checks that a company had written and recorded in its Cash account, but the checks have not yet been paid by the company’s bank (or have not “cleared” the bank). It is common for a few checks written in earlier months to remain outstanding at the end of the current month.

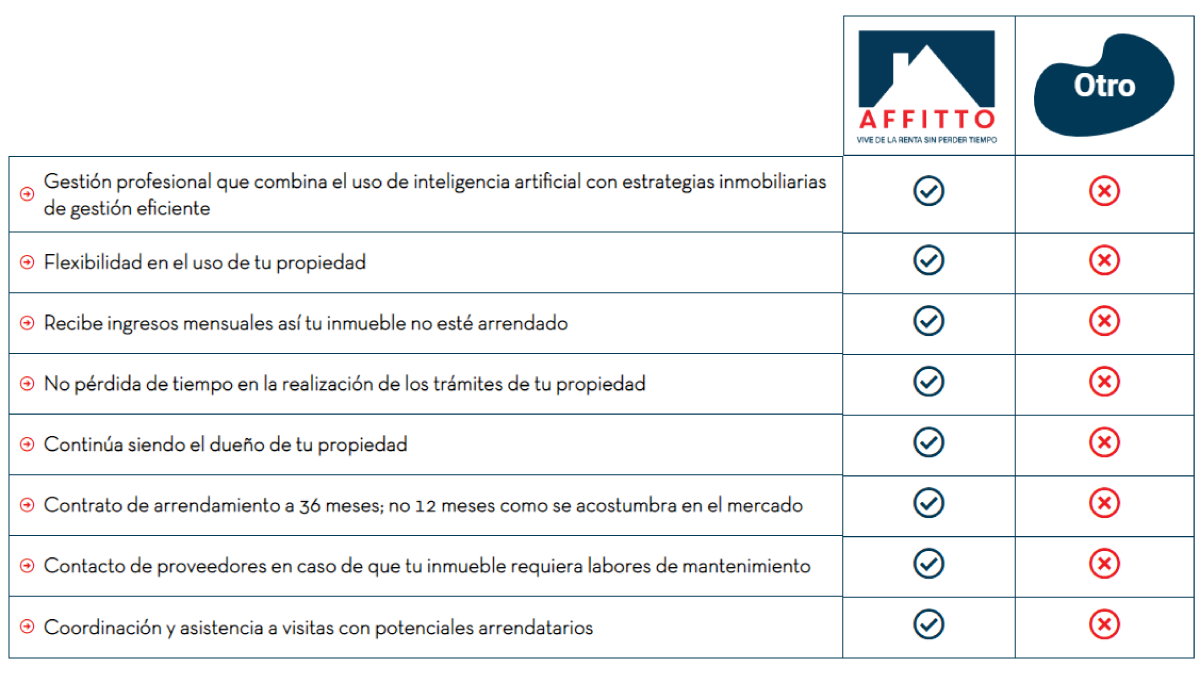

Permanencia: Por un periodo de 36 meses

Cuando aportas tu propiedad a Affitto te comprometes a que tu inmueble esté gestionado por nosotros por un periodo de 36 meses, podrás retirarte cumpliendo los periodos de notificación anticipada y cumpliendo con la penalización por terminación anticipada del contrato

Tareas que realiza Affitto

Nos encargamos de toda la gestión comercial y operativa de tu propiedad por medio de un equipo profesional que se apoya en tecnología avanzada: a.) Definición de la estrategia óptima de comercialización, incluyendo la definición del mejor canon de arrendamiento a cobrar, así como registros fotográficos, publicación en canales digital y físicos, muestra el inmueble a potenciales arrendatarios b.) Gestión operativa de tu propiedad, lo que incluye: 1.Relacionamiento con el propietario 2.Coordinación de mantenimientos y reparaciones 3.Cobro del canon de arrendamiento

Comisión de Affitto

Por la realización de nuestras labores (incluyendo comercialización y garantía del canon de arrendamiento mientras se encuentre vacante) cobramos una comisión del 20% sobre los ingresos brutos mensuales cuando el inmueble se encuentre arrendado.